Many apartment investors tell me they’ve paid off their debt years ago and have no need for a loan. While I applaud those debt-free investors for their prudence, I worry they could be leaving something on the table. One of the advantages of investing in real estate is that you can magnify your returns with low cost leverage. Let’s consider two investors: John and Trudy.

John invested in a 10-unit apartment in 1996. John purchased the investment with 30% down. John’s parents taught him the danger of having debt after they lost their home in a recession. As such, his goal was to pay off the loan as quickly as possible, so he used all excess cash flow to pay off the purchase loan.

Trudy invested in an identical 10-unit apartment in 1996. Trudy’s parents taught her that debt is not always bad, but in fact could be a useful tool when used wisely. Trudy purchased her property with 30% down as well. However, instead of paying down the loan with excess cash flow, she saved it and watched for new investment opportunities. All the while, she refinanced the loan whenever she could lock in a lower interest rate.

Fast forward to 2006. John continued to make extra principal payments, whereas Trudy built up a cash reserve waiting for the opportunity to buy in an overheating market. Then 2008 arrives and brings the Great Recession. John is grateful to have paid down his debt, and Trudy is grateful for her sizeable cash reserve. Trudy finds an investment opportunity in 2010 and buys a 10-unit apartment with 30% down using the accumulated cash. John also sees opportunities but doesn’t have nearly as much cash available for a down payment because he used most of his cash paying down his loan.

Fast forward again to 2019. Both investors have enjoyed tremendous appreciation. John paid off his loan a few years ago and is continuing to look for opportunities to invest in an increasingly pricey market. Trudy sees opportunity in the 30-60 unit space. She has built up significant equity in her properties, and she refinances those properties to access the equity and purchase her trophy asset: a 36-unit complex in a desirable neighborhood.

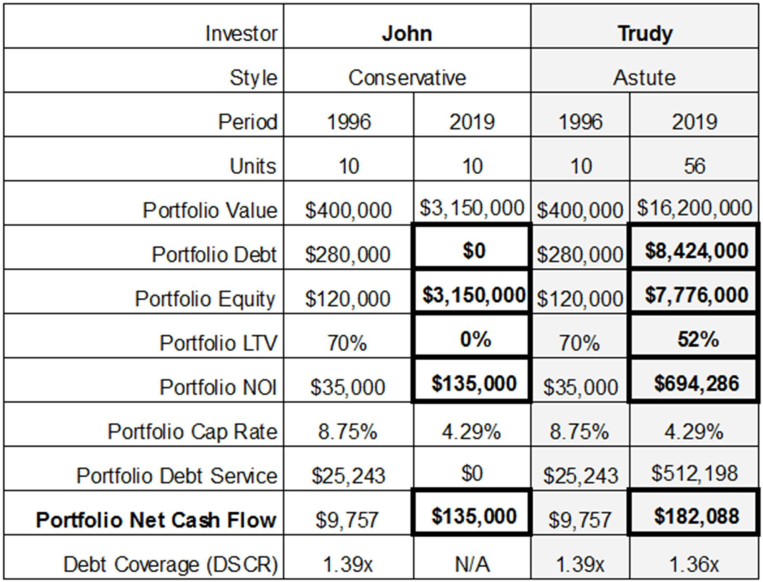

The table below shows where the two investors sit as of mid-2019:

John is in a respectable position with cash flow of $135,000 per year and no debt. He hasn’t expanded his portfolio, but now that he is debt free, John expects to accumulate cash flow quickly so that he is prepared for the next downturn.

On the other hand, Trudy has grown her portfolio from the identical 10-units as John to 56-units, including her trophy 36-unit investment. While she has debt against her portfolio, she is well positioned as evidenced by the 52% loan-to-value for her portfolio and 1.36x portfolio debt service coverage ratio. Not only does she generate about $47k more in net cash flow, but the debt service includes principal amortization that will increase her equity position every year.

Neither investor’s strategy is right for all investors as investing isn’t “one size fits all.” Some investors are more risk averse than others. It’s up to you to figure out where you sit on the risk-reward spectrum and act accordingly. Nonetheless, the parable of John and Trudy provides some key lessons about increasing our portfolio cash flow.

1. Refinance when rates decrease.

Pay attention to interest rates. When interest rates decrease, it may be a good time to refinance. Are you about to enter the adjustable period on your loan? If so, did you know that you’re likely to see an increase in the loan rate by 1-2%? It’s a good time to consider refinancing if your rate is adjusting or the interest rate to refinance is at least 50 bps lower than your current interest rate. Just make sure your current loan doesn’t have a prepayment premium that would eat up most of your savings. A good commercial mortgage broker will monitor your portfolio and let you know when it’s time to refinance.

2. Re-amortize your loan over 30-years.

If you are comfortable at your current debt level or leverage, consider interest-only loans and/or refinancing to reset your amortization schedule to 30-years. This approach reduces the amount of debt service going toward principal repayment, which increases your net cash flow.

3. Take out proceeds to buy new investments.

Take advantage of low-cost debt to purchase new investments and grow your portfolio. Refinancing allows you to access accumulated equity in your properties to purchase new investments. Real estate debt is generally the cheapest form of borrowing with the longest terms. This is because real estate is a relatively stable asset that generally appreciates. Consider that interest rates for apartment loans are in the high-3% to low-4% range today, whereas margin debt secured by stocks is typically in the 8%+ range. Furthermore, stocks are more volatile. A bad day in the stock market could lead to margin calls that would wipe out your equity. Real estate leverage is less risky provided you keep your LTV below 60% and your debt coverage above 1.35x.

Remember to structure your loans with full terms that match the amortization schedule. This means your loan doesn’t have a bullet maturity and instead it fully amortizes over say 30-years. Even if your interest rate adjusts over that period, the loan won’t mature and you can ride out a downturn without the risk of having your lender demand full repayment. A good commercial mortgage broker can explain these options if you have more questions.

4. Take out proceeds to paydown high interest rate debt.

Even if you don’t see any investment opportunities, you can draw on your equity to pay off debt with higher interest rates. Say you have borrowed against your stock portfolio at 8%. You could pay off that debt by refinancing a lowly levered property with a 4% interest rate. This would reduce your interest cost by half on that amount of debt. I have encountered many investors who could benefit from this strategy. Consider one investor who has two properties: one unencumbered property and a recent acquisition acquired with a hard money loan at 7.5%. If this investor refinanced the first property, he could generate enough proceeds to refinance the 7.5% hard money property with a lower cost conventional loan. He would go from paying 7.5% down to 4% simply by spreading the debt to a property with less debt.

Regardless of your debt appetite, there are opportunities for prudent investors to maximize their cash flow without taking additional risk. Review your portfolio today and check for opportunities to employ the four ideas above. If you have a commercial mortgage broker/advisor, discuss these ideas with them and ask if they see opportunities in your portfolio. Ideally, they should be reviewing your portfolio already and be reaching out to you!